This material originally appeared as a chapter in W. Bello and J. Chavez (eds.) State of Fragmentation: The Philippines in Transition. Bangkok: Focus on the Global South.

This entry is the last of a four-part serialization.

Part I

Part II: The new rules of the game

Part III: Back to the land

All told, the new Philippine economy saw billions of dollars churned into the land by overseas Filipinos and foreign investors, land that had been newly liberated from the state, agriculture, and domestic manufacturing, and redeveloped into subdivisions, condominiums, office space, and malls. This picture so far provides an account for what the new economy is, and why, how, and where these changes are taking place; what is so far lacking is an account of who benefited from this new economy.

As in any other economy, power in the brave new Philippines lies in the opportunities available for capitalist accumulation. Just like ownership of land under hacienda agriculture or dictatorial largesse under import-substitution industrialization, control over these opportunities will mean control over the creation of wealth.

The new economy saw, on one hand, the possibility of amassing wealth from haciendas or from small factories propped up by the state has been decisively closed off, even as important sunshine industries such as electronics manufacturing and business process outsourcing have daunting technical and financial entry barriers. On the other hand, the torrent of foreign investment and remittances that it has unleashed are creating immense opportunities in sectors which, whether by accident or design, are reserved for Filipinos.

Real estate development is one of these sectors. Over the past two decades, an array of crony capitalists, manufacturing-oriented taipans, and landed elites have converged on urban real estate as a central component of their strategies to diversify from their traditional sources of wealth. The ten richest Filipinos in 2012 all have interests in real estate; among the top 20, fifteen have significant holdings in real estate (See Table 6). Most of the real estate companies owned by these people and their families are fairly new to the game, and among this group, only Gotianun (Filinvest), Villar (Vista Land and Lifescapes) and Antonio (Century Properties) built their fortunes on real estate. The rest of the group is composed mainly of Chinese-Filipino taipans who built their wealth in manufacturing or retail, but with virtually zero investments in property development up until recently. The newest member of this group is Jollibee’s Tony Tan Caktiong, who in 2012 set up Double Dragon Properties with Mang Inasal’s Edgar Sia II. Up to this point, Tan Caktiong’s strategy of internationally expanding his fast food empire was becoming increasingly exceptional in a group composed of taipans that have taken the route of domestic intensification and diversification.

Table 6. Property development interests of the richest Filipinos.

| Rank, 2012[1] | Associated real estate companies[2] | Began operations | |

| Henry Sy and family | 1 | SM Development Corp.[3]

SM Prime Holdings Belle Corp. |

2003[4]

1985 1989 |

| Lucio Tan and family | 2 | Eton Properties Philippines, Inc. | 2007[5] |

| Enrique Razon, Jr. | 3 | Bloomberry Resorts and Hotels, Inc. | 2012 |

| John Gokongwei, Jr. and family | 4 | Robinsons Land Corp. | 1980 |

| David Consunji and family | 5 | DMCI Homes | 1999 |

| Andrew Tan | 6 | Megaworld Corporation

Empire East Land Inc. Global-Estate Resorts, Inc.[6] |

1989

2011 |

| Jaime Zobel de Ayala and family | 7 | Ayala Land, Inc. | 1948 |

| George Ty and family | 8 | Federal Land, Inc. | 1972 |

| Roberto Ongpin | 9 | Alphaland Corp.[7] | 2007 |

| Eduardo Cojuangco | 10 | San Miguel Properties[8] | 1990 |

| Tony Tan Caktiong and family | 12 | DoubleDragon Properties Corp.[9] | 2012 |

| Jon Ramon Aboitiz and family | 16 | AboitizLand, Inc. | 1993 |

| Andrea Gotianun and family | 17 | Filinvest Land, inc. | 1967 |

| Manuel Villar | 18 | Vista Land and Lifescapes, inc. | 1975[10] |

| Beatrice Campos and family | 19 | Greenfield Development Corp. | 1961 |

| Mariano Tan, Jr. | 22 | Greenfield Development Corp. | 1961 |

| Enrique Aboitiz and family | 23 | AboitizLand, Inc. | 1993 |

| Eric Recto | 24 | Alphaland Corp. | 2007 |

| Jose Antonio | 25 | Century Properties Group, Inc. | 1986 |

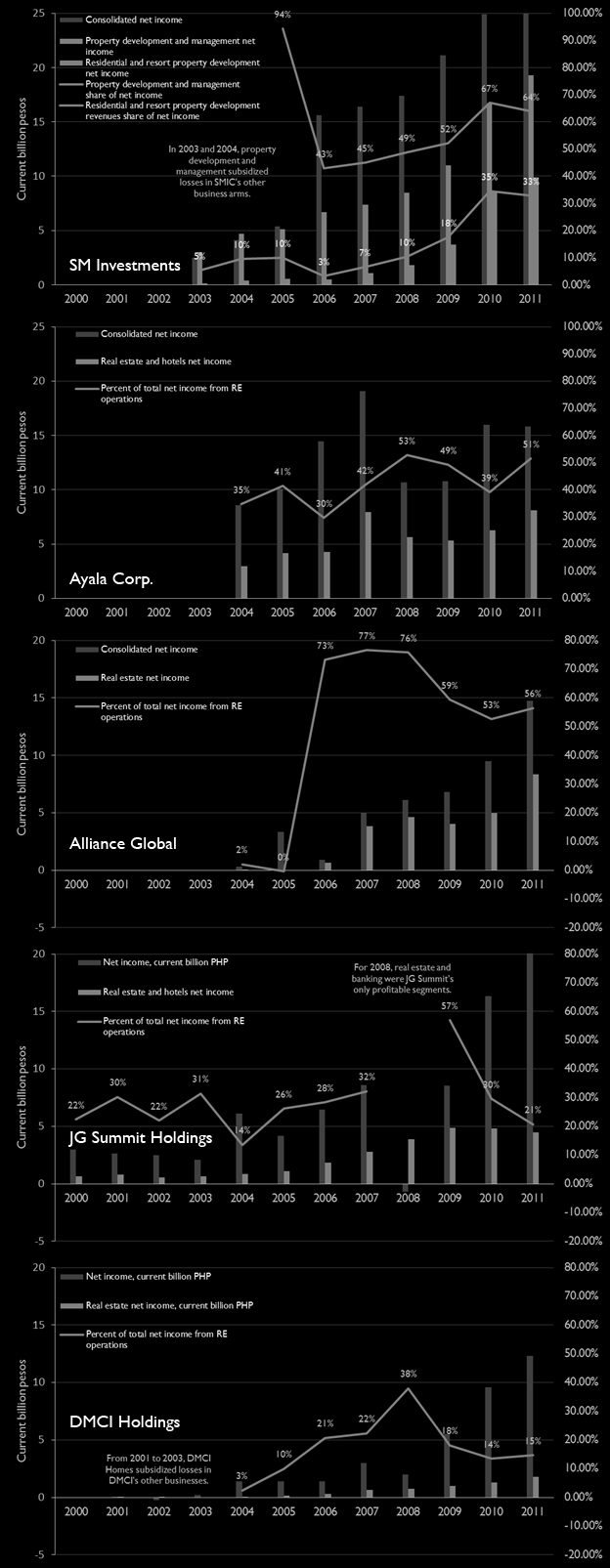

Despite being new entrants to the industry, these real estate companies now have a dominant position on the market, especially in the vertical development subsector. Henry Sy’s SM Development Corporation is perhaps the best example of this trend: with a market share of 23.8 percent, SMDC is now the largest condominium developer in the country, having sold some 28,650 units since its first construction in 2003.[11] It also comprises the fastest-growing arm of the Sys’ business empire: in 2006, housing and tourism development only accounted for 1 percent of the revenues of Henry Sy’s holding firm, SM Investments Corporation. By 2011, this had grown to 11 percent, and astoundingly accounted for a full third of SMIC’s profits. In contrast, retail—Sy’s bread and butter—brought in 76.6 percent of SMIC’s total revenues, but only accounted for 9.5 percent of total profits.[12]

The same story of rapid growth and incredible profitability repeats itself elsewhere: Andrew Tan’s Megaworld Corporation, which comes in at second place, completed its first project in 1994, now holds 13.1 percent of the market, and accounts for more than half of profits of Tan’s Alliance Global conglomerate. Lucio Tan’s Eton Properties completed its first project in 2007, now holds 5.2 percent of the market, and generated PhP4.45 billion in revenues in 2010 These giants also grew much faster than the already-impressive pace in the real estate sector: SM Development’s revenues grew by 47,400 percent from 2003 to 2011, while Megaworld’s grew by nearly 45,000 percent from 2004 to 2011. By the end of the decade, property development had been firmly established in the portfolios of the country’s largest conglomerates (See Figure 5).

Figure 5. The rapid growth of property development as an accumulation strategy. Share of property development in selected conglomerates’ net incomes from 2000-2011.[13]

At first pass, the newfound dominance of big capital in real estate development constitutes proof of the axiom that capital seeks its own level: that it will seek out the most profitable opportunities. Yet the opportunities available in real estate development were not available to just anyone: the specific contours of neoliberalism denied the participation of foreign firms, even as it created the conditions for these companies’ spectacular growth; it wasn’t merely generic capital which was able to exploit these conditions, but a specific fraction of it. Henry Sy’s dominance in real estate development and in banking owed as much to the protection afforded to him by foreign investment negative lists as it did to his ability to mobilize the requisite capital.

Part of the answer lies in the politics of neoliberalism. In understanding how neoliberalism ushered in a decade of super-profits for Filipino capitalists, a distinction made by David Harvey between neoliberalism as an ideological creed and neoliberalism as a project of restoring class power is useful. The former, which was underpinned by the ideas worked out by Friedrich von Hayek, Milton Friedman, and the so-called Austrian school of economics, and had since achieved hegemonic status within the academe, think tanks, and popular media, held that the well-being of individuals and of society are best advanced by “liberating individual entrepreneurial freedoms…within an institutional framework characterized by strong private property rights, free markets, and free trade.”[14]

Neoliberalism in practice, however, has shown a remarkable willingness to deviate from this ideal. Instead of reducing the perceived inefficient, distortive effect of the state on the economy, neoliberal reforms rely on the state’s monopoly over force to suppress dissent and organization against neoliberalism, and the state’s unique ability to create markets where there used to be none. Notwithstanding the Thatcherist “There Is No Alternative” mantra, three decades of neoliberalism has yet to engineer a global convergence on a single model of economic organization, but has instead produced a bewildering variety of place-specific neoliberalisms. In China, for instance, it had gone hand-in-hand with a strong state role in the creation of a new capitalist manufacturing class; across the Yellow Sea, meanwhile, it played a role in dismantling the cozy relationship between the state and the chaebol in South Korea.[15]

The one thing that has remained consistent across all variants of neoliberalism in all countries is that they have all created conditions for the re-concentration of class power that had been diluted under Keynesian-welfarist, developmentalist, and other political-economic projects enacted after World War II, all of which, to varying degrees, emphasized state involvement in tempering the excesses of capitalism.[16] This view of neoliberalism also accounts for the discrepancies between its theory and practice: a scriptural reading of the Austrian school would have forbidden China’s use of state power to enforce technology transfers from foreign investors to its domestic industries, and it wouldn’t have allowed Carlos Slim, presently the world’s richest man, to amass his fortune by monopolizing Mexico’s telecommunications market. If neoliberalism is understood as an excuse for the concentration of class power, and not as a coherent creed, these apparent sins suddenly make complete sense.

Under these conditions, diversification to real estate development emerged as an excellent strategy. As discussed in the previous sections, urban property development is neatly at the center of the new economy. Not only is it a shelter from the neoliberal storm, it is also well-positioned to salvage valuable flotsam: it is a sector protected from foreign competition, and a sector that stands to gain the most from the stagnation of agriculture through the development of greenfield sites for EPZs and suburban developments, and from the decline of the import-substitution industries by redeveloping brownfield sites for IT parks, malls, and residential towers. The technical barriers to entry are minimal, especially if competencies in construction, sales and marketing, and banking have previously been developed. The only major barrier is access to large amount of capital, which even works to their advantage as it insulates their companies’ operations from broader-based competition.

A direct consequence of this unevenness is that several sectors and industries have not only ended up being the exclusive domain of Filipino capitalists, but have enabled a resurgence of their class power. This is neither the ideal end result of neoliberal orthodoxy: compare the Philippines, for instance, against the rest of middle-income Southeast Asia, where foreign companies maintain a higher profile in the services sector. Britain’s Tesco has a dominant position in Bangkok’s retail landscape, and the biggest low-cost carriers in Malaysia, Singapore and Thailand are subsidiaries of Malaysia’s AirAsia. In these same sectors, the protection afforded by uneven neoliberalization had the consequence of creating unintentional national champions: SM, which began expanding internationally in 2001, and Cebu Pacific, which is presently the third-largest low-cost carrier in Asia.

Understood in this light, the specific contours of Philippine neoliberalization, as well as their outcomes, were not accidental. Neither were their consequences unalterable, intrinsic qualities of globalization. Instead, they reflected the exercise of power to effect specific outcomes, not only through SAPs implemented by the international financial institutions and the ideological support of Filipino technocrats, but also by political elites and domestic capitalists.

Nowhere is the fusion of business and politics in urban land more apparent than in Congress. Members the landed and political cacique classes, eager to avoid agrarian reform, have also cashed in the demand for suburban house-and-lot developments, industrial zones, cemeteries, and resorts by converting their landholdings, and in many instances by participating in the development business as well. Research by Sheila Coronel and the Philippine Center for Investigative Journalism showed that, from 1992 to 2004, the proportion of congressmen and women with agricultural land dwindled from 58 to 39 percent. The proportion that had interests in real estate remained steady, from 53 to 49 percent. In the 9th Congress, agricultural land was the dominant business interest in the lower house, as it had been historically: by the 11th Congress, real estate development replaced it at the top spot.[17]

As with hacenderos in pre-Marcos Congresses, this is a potent lobby that shows no qualms with using political power to protect its interests. Thanks to decentralization of key decision-making processes, they are able to exploit the unclear boundaries between patrimonial and public powers at the local level to help the process of land conversion along.[18] In Congress, they have voted to increase the funds granted to the National Home Mortgage Finance Corporation through the Comprehensive and Integrated Shelter Financing Act.[19] Beginning with Juanito Remulla’s lobbying of Marcos, who was his fraternity brother, to locate an export processing zone in Cavite,[20] particularly influential politicians have been able to leverage their power for the declaration of special economic zones in their fiefdoms, the prioritization and realignment of national infrastructure projects which serve these zones. To varying extents, influence in Malacañang and with other lawmakers certainly helped the declaration of pet-project economic zones in Zamboanga, Cagayan, and Aurora, and the realignment of expressway projects in southern Manila and Central Luzon.

Senator Manuel Villar perhaps presents the prototype of the 21st-century panginoong may-lupa: a real estate developer who was able to build on his business to ‘diversify’ into politics, and then eventually exploit synergies between the two. Villar had been implicated in a number of allegations of land-grabbing in Bulacan and Cavite and the use of pork barrel funds to fund roads serving developments put up by his company, Vista Land and Lifescapes (VLL), and had been the subject of a Senate ethics investigation on his involvement in the realignment of the C-5 extension expressway project to benefit VLL developments;[21] meanwhile, in the 16 years between winning his first election in 1992 and his 2008 presidential bid, Villar’s net worth grew by thirteen times its original size.[22] *

The creative destruction of Filipino capitalists

Another key feature of the new urban property landscape that needs to be examined is how and why not all of the established real estate companies have been able to benefit from this boom: among the old guard, Ayala Land, Vista Land and Lifescapes, and to a certain extent Filinvest fared much better than companies such as Fil-Estate, Sta. Lucia, and New San Jose Builders. Historically, real estate has proven itself as the most resilient moneymaking machine in the country. Owing to the high and relatively secure returns, urban land speculation has long been a favored accumulation strategy not just by elites, but also by middle classes.[23] Between 1975 and 1991, urban land appreciated at a rate of 2.5 to 3.65 times faster than the GDP growth rate.[24] As a consequence, as late as 1991, 44 percent of all urban land in Metro Manila was held by a few elite families;[25] virtually all fractions of domestic capital have, to varying extents, investments in land speculation.[26] Yet as the recent jostling for the land held by the Ortigas clan between the SM and Ayala conglomerates demonstrate, there is a qualitative difference between family-owned estates held as idle speculative assets and land bank for property development; whichever conglomerate ends up acquiring the land, the true winner will be diversified capital, and the true loser will be landed, speculative capital. The large landowning families of Metro Manila, such as the Ortigases, the Aranetas, and the Tuasons, are no longer major players in property development; this indicates that the property development industry isn’t merely different in the scale of capital it now involves, but is also a qualitatively different game.

The story of Ayala Land might provide some insight into how the game has changed. Among the major capitalist clans of the Philippines, the Ayalas were the first to discover that skyscrapers were much more valuable crops than sugar. The family initially built its wealth in an industry allied to cash crops—liquor distillation—and then forayed into insurance during the American colonial period. After the Second World War, they began developing its landholdings in Hacienda Makati in earnest: beginning with the development of Forbes Park in 1948, it set about on a long-term development project which would eventually lead to the development of the Makati Central Business District, and by the 1960s the Ayalas were the country’s largest real estate developer.[27] For the rest of the century, property development remained the core business of the family, even as it diversified into businesses such as banking, automotive sales, food processing, electronics manufacturing, and most recently, business process outsourcing. The past decade also saw Ayala Land diversify beyond its high-income mainstay business into middle- and even low-income housing, and the company launched a record number of units in 2010 and 2011.

This story illuminates two processes defining how Filipino capitalism and urban property development are both changing. With some variations, the trajectory taken by a number of other capitalists in recent years mirror those taken by the Ayalas. Up to the mid-nineties, the core businesses of John Gokongwei, Jr., Andrew Tan, and Lucio Tan were manufacturing industries closely allied to cash crops, such as sugar refining, food processing, liquor distillation, and cigarettes. Lucio Tan began in tobacco, with substantial help from Marcos, acquired La Tondeña in the late eighties, and then began to aggressively diversify into services in the 1990s. The situation of the Gokongwei’s JG Summit is particularly illuminating as, over the past decade, Robinsons Land had been the only consistently profitable arm of the conglomerate, and JG Summit had actually closed its textiles operation in 2006.[28] Incidentally, the only conglomerates described by Yoshihara in his 1988 study which are thriving today are those involved in liquor and food processing, such as La Tondeña, San Miguel, and Universal Robina, or those which have operations in the services industry, particularly retail and banking; without exception, all of these conglomerates have diversified into real estate.

At the same time, the diversification of Ayala Land into multiple market segments demonstrates a shift in the urban property sector itself. To take advantage of the property boom, it was no longer sufficient to merely have a large land bank, or to have a history in real estate development; what became the overriding qualification was the ability to mobilize large amounts of capital to meet the globalized sources of demand, which are demanding altogether different sorts of products—condominiums, IT offices, and export processing zones—from the ones offered by traditional developers. The cash-flush conglomerates of the taipans had this ability; the previously-dominant developers did not.

As argued by Neil Brenner and Nik Theodore, neoliberal reform must be understood as the outcome of a dialectical process of the neoliberal project with “legacies of inherited institutional frameworks, policy regimes, regulatory practices, and political struggles.”[29] They never arrive at an ideologically-pure form of neoliberal practice, but rather at path-dependent and locally-specific reconfiguration of interests and institutions, a “creative destruction” that involves “the (partial) destruction of extant institutional arrangements and political compromises through market-oriented reform initiatives; and the (tendential) creation of a new infrastructure for market-oriented economic growth, commodification, and the rule of capital.”

This process is revealed by looking at the similarities and differences between the old and the new economy. The first and most obvious similarity and difference is that Filipino capitalists are going back to land as a source of wealth, but instead of utilizing it as a base for a rural, cash crop-oriented economy, it is being used for urban development. Urban development is itself being reconfigured: while it remains a lucrative investment, profits from it are now realized through its active circulation as capital, as opposed to speculation of idle assets. But beyond this, the framework also illuminates other aspects of Filipino capitalism in the 21st century. For one, a number of prominent names and families retained their wealth and dominance over the Philippine economy. What needs to be recognized, however, is that while they may be the same people or come from the same families, they now belong to an altogether different fraction of capital. These changes demonstrate a need to shift the discussion from who our capitalists are—what their racial backgrounds are, how they lead their lives, who their kids marry, and all such other lifestyle section prattle, ad nauseam—into what our capitalists are. From some angles, they may resemble their comprador forebears, in that they accrue profits from globalized (née foreign) sources of demand, and can become immensely wealthy without improving the lives of the rest of Filipinos. But in contrast to the compradores, 21st century Filipino capitalists, fueled by remittances and foreign investment, are accumulating a war chest to transform themselves into a truly transnational class.

The question, now, is if this mode of capitalist growth can translate into broader-based gains, as seen for examples in the rest of East Asia. This leaves us with one final aspect of the Filipino capitalists’ creative destruction: in a manner similar to the keiretsu of Japan and the chaebol of South Korea, a nationally-contingent species of transnational conglomerates is being formed in the Philippines. However, in contrast to their East Asian counterparts, Filipino capitalists are becoming transnational without even becoming substantively industrial, or more specifically, without neither a developmental commitment with the state nor a Fordist incentive to create a strong domestic market nor a partnership with labor. If they can profit now without having to ensure the improvement of the lives of Filipinos, there is no reason to believe that they will in the future.

[1] Rankings derived from Forbes (2012). Philippines’ 40 Richest List. Retrieved 17 May 2013 from http://www.forbes.com/philippines-billionaires/list/

[2] Firms operating in distinctly different segments, and/or are not structured as subsidiaries of another property development firm within the conglomerate, are listed; subsidiary brands, e.g. Alveo, Avida, and Amaia for Ayala Land, Inc., are not listed as separate entities.

[3] SM Development Corporation was consolidated with SM Prime, SM Investment Corporation’s mall development arm, in May 2013.

[4] Date of first construction. SM Development itself was acquired, as Ayala Fund Inc., in 1986, and renamed SM Fund Inc. It was renamed SMDC in May 1996.

[5] Date of first construction in the Philppines. Lucio Tan’s Eton Properties was first established in Hong Kong in the 1980s, where its business is worth US$ 2.6 billion. http://business.inquirer.net/75247/biz-buzz-buying-air-rights

[6] Formerly Fil-Estate Land, Incs., acquired by the Alliance Global Group in 2011. See Dumlao, D. (2011). “Alliance Global takes 60% control of Fil-Estate Land.” Philippine Daily Inquirer, 12 January 2011. Accessed 17 May 2013 from http://business.inquirer.net/money/breakingnews/view/20110112-314057/Alliance-Global-takes-60-control-of-Fil-Estate-land.

[7] Joint venture with Ashmore Group, a London-based private equity fund, and Ongpin’s RVO Capital Ventures Group.

[8] Through San Miguel Corporation, although Mr. Cojuangco divested of his stake in San Miguel Corporation in mid-2012.

[9] Founded as a joint venture with Edgar Sia II of Mang Inasal.

[10] As Camella Homes. Vista Land and Lifescapes incorporated 2006.

[11] Data sourced from SM Development Corporation (2011). SM Development Corporation – Company Presentation, April 2011; SM Development Corporation (2001-2011). SM Development Corporation Annual Report.

[12] SyCip Gorres Velayo & Co. (2012). Independent Auditor’s Report, SM Development Corporation, p. 35.

[13] Data sourced from the annual reports of these conglomerates from 2000 to 2011.

[14] Harvey, D. (2005). A Brief History of Neoliberalism. Oxford: Oxford University Press, p. 2.

[15] For a discussion of neo-liberalism in Korea, see Pirie, I. (2006) “Economic crisis and the construction of a neo-liberal regulatory regime in Korea.” Competition and Change, 10(1):49-71.

[16] Harvey, D. (2005). A Brief History of Neoliberalism. Oxford: Oxford University Press, pp. 19-36.

[17] Coronel, S. (2003). “Open for Business.” i Magazine, 9(3). Retrieved 14 May 2013 from http://i-site.ph/Analysis/business.html

[18] Kelly, P. (2003). “Urbanization and the Politics of Land in the Manila Region.” The Annals of the American Academy of Political and Social Science , 170-187.

[19] Coronel, S. (2003). “Open for Business.” i Magazine, 9(3). Retrieved 14 May 2013 from http://i-site.ph/Analysis/business.html

[20] McKay, S.C. (2006). Satanic Mills or Silicon Islands? The Politics of High-Tech Production in the Philippines. Ithaca: Cornell University Press , p. 143.

[21] Torres, T. (2011). “SC gives green light for Senate to probe Villar on C-5 road allegation.” Philippine Daily Inquirer, 14 March 2011. Retrieved 10 May 2013 from http://newsinfo.inquirer.net/inquirerheadlines/nation/view/20110314-325418/SC-gives-green-light-for-Senate-to-probe-Villar-on-C-5-road-allegation

[22] Collas-Monsod, S. (2010). “Who junked compassion and decency?” Philippine Daily Inquirer, 9 April 2010. Retrieved 10 May 2013 from http://opinion.inquirer.net/inquireropinion/columns/view/20100409-263313/Who-junked-compassion-and-decency.

[23] Goss, J. (1998). “The Struggle for the Right to the City in Metro Manila.” Philippine Sociological Review, 46(3-4), pp. 88-120.

[24] Bautista, M.C.R. (1998). “Culture and Urbanization: the Philippine Case.”

[25] Berner, E. (1997). Defending a Place in the City: Localities and the Struggle for Urban Land in Metro Manila. Quezon City: Ateneo de Manila University Press, p. 21.

[26] Krinks, P. (2002). The Economy of the Philippines: Elites, Inequalities and Economic Restructuring. New York: Routledge, pp. 199-201; (1994). Landlords and Capitalists: Class, Family, and State in Philippine Manufacturing. Quezon City: University of the Philippines Press, p. 33.

[27] Batalla, E.V. (1999) “Zaibatsu Development in the Philippines: the Ayala Model.” Southeast Asian Studies, 37(1): 18-49.

[28] JG Summit Holdings, Inc. (2007) 2007 Annual Report, p. 122.

[29] Brenner, N. and Theodore, N. (2002). “Cities and the Geographies of “Actually Existing Neoliberalism.” In Brenner, N. and Theodore, N. (eds.) Spaces of Neoliberalism: Urban Restructuring in North America and Western Europe. Oxford: Blackwell.