This material originally appeared as a chapter in W. Bello and J. Chavez (eds.) State of Fragmentation: The Philippines in Transition. Bangkok: Focus on the Global South.

This entry is the second of a four-part serialization.

Part I

Part III: Back to the land

Part IV: The creative destruction of Filipino capitalists

From the early 1980s to the present, the structure of the Philippine economy, its position astride global circuits of labor, commodities, and capital, and the opportunities for accumulation available to its capitalist classes have been defined by three sets of processes. First among these was neoliberalization. At first glance, the Philippines was perhaps one of the countries where neoliberalism saw an unqualified ideological triumph. It was among the first countries in the world to participate in structural adjustment program in 1980, and has since been the recipient of a total of nine structural adjustment loans from the World Bank and a participant in three IMF programs.[1] The momentum of neoliberal reform has been sustained from within by state economic planning agencies, the academe, and private-sector think tanks.[2] As a consequence, the Philippines has consistently gone above and beyond the prescriptions of the Washington Consensus: it had unilaterally adopted among the lowest average tariff rates in the world, innovated the privatization of economic zones, and embarked on some of the biggest privatizations in the world.

Far from being a completely ideological project, however, neoliberalization in the Philippines has been implemented in a specific, locally-contingent, and highly-uneven manner, and the resultant contours were crucial to the recent successes of domestic capitalists. This is perhaps most evident in the Philippine privatization program. Beyond the crown jewel corporations, such as Philippine Airlines, Petron, National Steel, and Napocor, public land and infrastructure have been the most consistent targets for privatization by successive post-EDSA governments. In Manila, the privatization of military-owned land, such as Fort Bonifacio and Camp Bago Bantay, of national government centers in Quezon City, and of reclaimed land on Manila Bay have in recent years been a defining feature of urban development in the city. Through the Bases Conversion and Development Authority alone, a total of 267 hectares in the city have been privatized in this manner, creating some PhP46.697 billion in revenues.[3]

Two particular features of the privatization program deserve closer scrutiny. The first feature is that these privatizations were pursued through auctions of large tracks of land. This is not the only means through which privatization can be accomplished: the privatization of Singapore Airlines, for instance, was accomplished through a public offering, which allowed the Singaporean middle class to participate in the privatization process.[4] As another conjectural alternative, the land assets of the national government could also have been privatized as smaller lots, or allocated for socialized housing. In the manner in which these assets were privatized, however, the lots were huge, and the stakes high. The mandate of the Bases Conversion and Development Authority (BCDA) to sell the land at as high a price as possible has meant that these parcels were sold for the highest bids, precluding the use of these lands for anything but the highest ends of the market. The initial bloc of Fort Bonifacio that was privatized in 1995 was 150 hectares, and the winning bid was a hefty US$1.6 billion. As of writing, the highest bid for the latest parcel to be privatized, the 74-hectare FTI Complex in Taguig, was PhP24.3 billion.[5] To put this figure in perspective: under the Urban Housing and Development Act, the mandated maximum size for socialized housing house-and-lot units, which have a price ceiling of PhP400,000 per unit, is 18 square meters. At the prices paid by the winning bidders, an unimproved 18 square-meter plot in Fort Bonifacio would cost PhP676,962 and PhP591,081 in the FTI complex. No wonder, then, that the privatized Fort Bonifacio is now a master-planned high-end district whose recent locators include the embassies of Singapore and the United Kingdom, the new headquarters of the Philippine Stock Exchange, and the local offices of several multinational corporations.

The second feature is that these privatizations took place with the national patrimony provisions of the 1987 Constitution firmly in place, which limited foreign ownership of private land to 40 percent of total equity. These provisions have often been understood in terms of resistance to the neo-colonial appropriation of the country’s natural resources: Filipino resources should benefit Filipinos, or so it was thought. But given the highest-bidder, winner-take-all system in place for privatizing land, and the constitutional restrictions on land ownership, this system effectively enforced an oligopoly for Filipinos who could effectively mobilize the capital, either their own, or that of foreign partners (see Table 2).

TABLE 2. Major land privatizations and public-private partnerships in Metro Manila, 1995 to 2010.

The same unevenness was also apparent in the pace and shape taken by trade liberalization and deregulation in the country. On one hand, trade liberalization was remarkably brutal to agriculture and industry, as has been described above. On the other, several key sectors were protected from complete foreign ownership to varying degrees, guaranteeing a place in the economy for domestic capital. As with private land, foreign equity in mining companies and public utilities—including telecommunications—was limited to 40 percent of total equity. For banks, the limit was 60 percent. Retail trade was likewise liberalized, but in a halting and piecemeal manner: high-capitalization stores can put up with foreign equity, but they had to rent space in malls, which cannot be foreign-owned. But the extent to which Philippine administrations would bend neoliberal doctrine backwards for favored parties is best demonstrated in the airline industry, when in 1998 Joseph Estrada rolled back an earlier open skies policy to shield Philippine Airlines, then majority owned by his friend Lucio Tan, from foreign competition.[16]

Elsewhere, the Philippines was innovating new forms of liberalization which again opened opportunities for Filipino capitalists. In 1995 it was the first in the world to transfer the development and administration of export-processing zones, which had heretofore been the exclusive domain of states, to the private sector.[17] In 2000, it allowed single floors of buildings to be declared as information and communications technology (IT) special economic zones, which would pave the way for the rise of the multi-billion dollar business process outsourcing (BPO) industry. These innovations have meant that the export processing zone program of the Philippines has been one of the most successful globally, and from 2005 to the 2010, the Philippine Economic Zone Authority (PEZA) recorded IT investments totaling 10 billion dollars.[18] The national patrimony provisions of the constitution, however, assured that the few Filipinos who could mobilize the requisite capital had at least a 60 percent stake in the development and operation of these zones.

Uneven neoliberalization also played a role in realizing the second set of processes: the specific form that economic globalization has taken in the Philippines, which has specialized to fulfill three clear niches in the global economy. The first among these is in electronics manufacturing, primarily in the low value-added, labor-intensive processes of testing and sub-assembly manufacturing. Since 1997, electronics have consistently accounted for more than half of all commodity exports of the Philippines, and the value of electronics exports have grown from US$22.17 billion in 2000 to US$31 billion in 2010.[19] This growth, however, has taken place almost entirely within export processing zones, and with some exceptions such as the Ayalas’ Integrated Microelectronics Inc. (IMI), this industry has seen very little participation by domestic capitalists[20]—other than, of course, the development and administration of the zones themselves.

The growth of services outsourcing has been the second success story of the new Philippine economy: virtually nonexistent in 2000, by 2010 the industry was raking in US$9.5 billion in exports earnings and employing a little more than half a million people.[21] From 2004 to 2010, revenue growth in the sector averaged 54 percent annually, and the Philippines is now one of the biggest services outsourcing destinations in the world. But as with the export electronics industry, outsourcing as a whole is dominated by low value-added activities, particularly call centers. Domestic capitalist involvement is likewise limited to the development and rental of office space for the locators, with foreign equity representing 92 percent of total equity for the entire industry in 2009.[22]

Finally, the weak record of domestic employment generation in the neoliberal era has underpinned a massive labor exodus, and labor export and remittances comprise an outsize proportion of economic activity in the country. In 2010, out of a labor force of 37.1 million, 1.9 million Filipinos were deployed overseas on temporary contracts.[23] During the same year, remittances totaled 18.76 billion US dollars, the fourth-largest inflow of remittances in the world after India, China, and Mexico. This exodus had come at an immense social and human cost, but had been invaluable in keeping the Philippine economy above the water during the present financial crisis: as most analyses have pointed out, domestic consumption in the services sector, not export growth nor investment, has been the motor of the Philippines’ recent above-average economic performance (see Figure 1).

Figure 1. Overseas Filipino remittances, electronics exports, and IT-BPO exports, 2000 – 2010[24]

A final set of factors have ensured that this very same economic performance failed to substantively improve the well-being of the majority of the Filipinos, but at the same time created spectacular profits for Filipino capitalists: the sectoral and geographical unevenness of capitalist development. With stagnation in agriculture and a weak transition to export-oriented industrialization, the past three decades saw the services sector dominate the Philippine economy. By 2010 it accounted for 55 percent of the country’s GDP and a little more than half of total employment. Among the sectors which were able to outpace the growth of the economy from 2000 to 2010, only bananas and fisheries were agricultural, and the only industrial subsector was mining.[25] But as with the case of the postindustrial societies of the global North, the growth in services created a bifurcation of opportunity: on one hand, remittance and outsourcing work are creating narrow culturally- and economically-globalized middle classes; on the other, the low-wage, flexibilized services jobs sustaining the economy are performed by a large and growing precariat. Remittances have had the effect of exacerbating this situation: while the early phase of labor export saw remittances being used to sustain agricultural livelihoods, OFW expenditures have since shifted to education, consumption, and investment into real estate.[26]

Geographically, the transformation of the economy had favored Manila and its surrounding regions. The sectors which the Philippines had established a niche in are overwhelmingly urban in character: in 2011, NCR, Central Luzon and Calabarzon deployed 43.3 per cent of the country’s overseas workforce;[27] meanwhile, data from the 2007 Family Income and Expenditures Survey show that 93.9 per cent of remittance-receiving families from these regions have incomes of PhP100,000 or higher.[28] This should not come as a surprise, given the very high upfront costs involved in deploying overseas for work would mean that it will be the better-off families in the better-off regions, and not the poorest of the poor, who would benefit from overseas remittances. The employment that had been generated by export-oriented manufacturing has concentrated in peri- and exurban greenfield sites in Cavite and Laguna, where they can be assured of a steady power and water supply, access to the airport in Manila, and a compliant labor force policed by the local government.[29] Lastly, the BPO boom had concentrated in the business districts of Manila: before the enactment of a provision which allowed single floors of office space to be declared as special economic zones, Manila had zero economic zones. By the end of the decade, the number had jumped to 82.

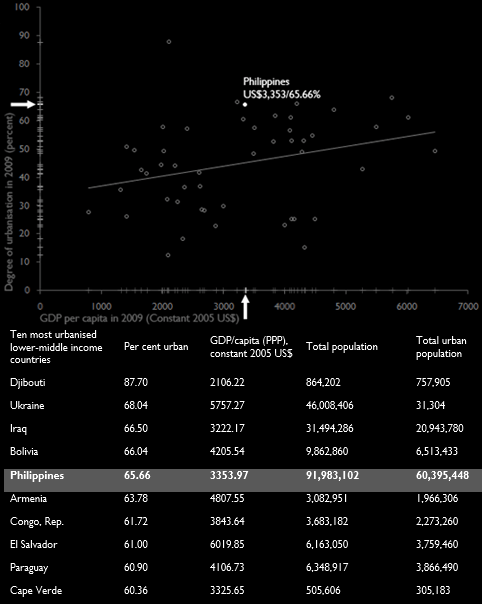

Jobs and opportunities were therefore being concentrated in the cities, even as the viability of rural, agrarian livelihoods was increasingly rendered tenuous. Pre-existing push and pull factors for rural-urban migration have been exacerbated, creating a level of urbanization in the Philippines that is anomalously high for the level of development. Among the 56 lower-middle income countries classified by the World Bank, the Philippines has the fifth-highest level of urbanization, and its urban population is larger than the rest of the top ten combined (see Figure 2). Manila, which has historically been the primate city of the Philippine urban system, has been the primary destination of this rural-urban exodus. Over the past decade, a trend of economic decentralization from the core of Manila to its surrounding regions had been reversed, and the share of its greater city-region in the Philippine economy has consistently remained above fifty percent of GDP.

Figure 2. Urbanization v. GDP/capita for lower-middle income countries, 2009[30]

Part I

Part III: Back to the land

Part IV: The creative destruction of Filipino capitalists

[1] Bello, W. (1999) “Is the Structural Adjustment Approach Really and Truly Dead?” Transnational Institute. Retrieved 17 February 2013 from http://www.tni.org/article/structural-adjustment-approach-really-and-trully-dead

[2] Bello, W., de Guzman, M., Docena, H., & Malig, M. (2004). The Anti-Development State: The Political Economy of Permanent Crisis in the Philippines. Quezon City: University of the Philippines Press, pp. 92-95.

[3] Bases Conversion and Development Authority (2010). Annual Report 2010: Setting New Goals, Charting New Directions, p. 33.

[4] Bowen, J. T. and T. R. Leinbach (1995) “The State and Liberalization: the Airline Industry in the East Asian NICs.” Annals of the Association of American Geographers, 85(3):468-493.

[5] Camus, M.R. (2012). “Ayala overbid on FTI not so drastic.” Business Mirror, 30 August 2012.

[6] Gonzales, I.C.C. and Visto, C.S. (2004). “SM unit buys Bago Bantay property for P695 million.” BusinessWorld, 19 February 2004.

[7] Ibid.

[8] Osorio, M.E.P. (2008). “Rufino group bags ‘primest lot’ in Global City for P2.032B.” Philippine Star, 29 April 2008.

[9] Camus, M.R. (2012). “Ayala overbid on FTI not so drastic.” Business Mirror, 30 August 2012.

[10] Lorenzo, A.B.L. (2007). “Metropac on Fort Bonifacio: biting off more than it could chew.” BusinessWorld 2007 Anniversary Report, 26 July 2007.

[11] Bases Conversion and Development Authority (2010). Annual Report 2010: Setting New Goals, Charting New Directions.

[12] Ibid.

[13] Bases Conversion and Development Authority (2009). Annual Report 2009: A Catalyst for Transformation.

[14] Dumlao, D. (2012). “Ayala Land unveils P65-B business district project in QC. Philippine Daily Inquirer, 5 July 2012. Retrieved 13 May 2013 from http://business.inquirer.net/69289/ayala-land-unveils-p65-b-business-district-project-in-qc.

[15] Bases Conversion and Development Authority (2010). Annual Report 2010: Setting New Goals, Charting New Directions.

[16] Bello, W., de Guzman, M., Docena, H., & Malig, M. (2004). The Anti-Development State: The Political Economy of Permanent Crisis in the Philippines. Quezon City: University of the Philippines Press, pp. 247-249.

[17] McKay, S.C. (2006). Satanic Mills or Silicon Islands? The Politics of High-Tech Production in the Philippines. Ithaca: Cornell University Press, pp. 150-154.

[18] Bangko Sentral ng Pilipinas (2010). Results of the 2010 Survey of Information Technology-Business Process Outsourcing Services. Retrieved 28 February 2013 from http://www.bsp.gov.ph/downloads/Publications/2012/ICT_2010.pdf.

[19] National Statistics Office (1977-2010). Philippine Statistical Yearbook.

[20] McKay, S.C. (2006). Satanic Mills or Silicon Islands? The Politics of High-Tech Production in the Philippines. Ithaca: Cornell University Press, p. 56.

[21] ABS-CBNNews.com (2012) “IT-BPO revenues hit $10.1 billion in 2010. ABS-CBN News. Retrieved 28 February 2013 from http://www.abs-cbnnews.com/business/04/06/12/it-bpo-revenues-hit-101-billion-2010.

[22] Bangko Sentral ng Pilpinas (n.d.). Foreign-to-Total Equity Ratio by IT-BPO Category, 2005-2009. Retrieved 28 February 2013 from http://www.bsp.gov.ph/statistics/keystat/ict/itbpo_3.2.htm

[23] National Statistics Office (2009; 2010). Philippine Statistical Yearbook. Quezon City: National Statistics Office.

[24] Data from the National Statistical Coordination Board (various years). National Accounts of the Philippines.

[25] Banzon-Bautista, C. (1989). The Saudi Connection: Agrarian Change in a Pampangan Village, 1977-1984. Agrarian Transformations: Local Processes and the State in Southeast Asia. Berkeley: University of California Press. pp. 144-158; Bangko Sentral ng Pilipinas (2007-2013). Consumer Expectations Survey.

[26] National Statistics Office (2012). 2011 Survey on Overseas Filipinos.

[27] Institute for Migration and Development Issues (2008).”Table 62: Regional data of families receiving cash, gifts and other forms of assistance from abroad Family Income and Expenditures Survey (FIES)” Philippine Migration and Development Statistical Almanac. Retrieved 14 May 2013 from http://almanac.ofwphilanthropy.org/index.php?option=com_content&task=blogcategory&id=104&Itemid=122

[28] Remittances and IT-BPO exports data from Bangko Sentral ng Pilipinas (n.d.) Economic and Financial Statistics. Retrieved 29 February 2013 from http://www.bsp.gov.ph/statistics/efs_ext3.asp. Electronics exports data from National Statistics Office (2000-2010) Philippine Statistical Yearbook.

[29] McKay, S.C. (2006). Satanic Mills or Silicon Islands? The Politics of High-Tech Production in the Philippines. Ithaca: Cornell University Press, pp. 146-165.

[30] Data derived from The World Bank (2012). World Development Indicators and Global Development Finance. Washington, D.C. Retrieved 20 February 2013 from http://databank.worldbank.org/ddp/home.do.